Global

Global Singapore

Singapore United States

United States Hongkong

Hongkong Group

GroupSummary:

In the latest FOMC Meeting held 02nd November, the Federal Reserve raised rates by 75 basis points for the fourth consecutive time. The Fed Funds Rate now sits at 3.75% -4%. Importantly, key takeaways from November’s meeting include:

MACRO MARKETS

1、Fed Goes Hard Again

In the latest FOMC Meeting held 02nd November, the Federal Reserve raised rates by 75 basis points for the fourth consecutive time. The Fed Funds Rate now sits at 3.75% -4%.

Source: Bloomberg

Source: Bloomberg

Key Takeaways:

Higher Terminal Rates on the card

Since its September’s forecasts, the committee was said to have revised upwards its assessment of the terminal federal funds rate. Greater clarity will nevertheless be obtained when the Fed releases a new dot plot next month, although expectations are for the median rate to be approaching 5%.

Implied Slowing of Future Rate Hikes

While Fed Chair Jerome Powell made no explicit response to whether a 50-basis points hike was up and coming, he did point out that the process of “frontloading” was in huge part completed and acknowledged the lags in monetary policy. Separately, the Fed’s reference to “financial developments” further indicates its concerns surrounding financial stability.

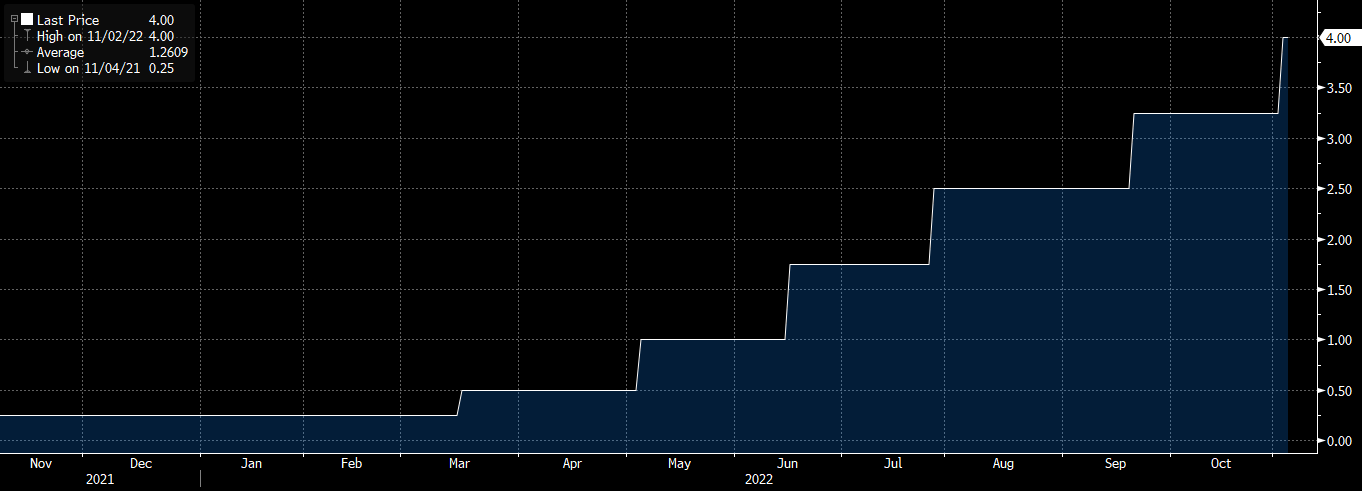

2、Treasury Yield Curve Inversion Unlocks New High

Source: Bloomberg

Source: Bloomberg

The inversion of the two and ten-year treasury yield curve has touched a new level. As of 03rd November, two-year yields surpassed the ten-year’s yield by as much as 58.6 basis points. This more than surpassed the 58 basis points last witnessed approximately four decades ago.

A yield curve inversion takes place when shorter-term bonds, which are highly policy-sensitive, generate higher returns than longer-dated bonds. As such, it is not surprising for inversions to take place given that the Fed has been highly adamant about bringing down inflation in the past year alone.

While inversions are perceived negatively by most since history has proved that they precede a recession by twelve to eighteen months, these inversions are likely to stay. Reason being that any bullishness seen in macroeconomic data releases moving forward could potentially lead to increased yields and subsequent inversion occurrences.

3、Nonfarm Payrolls Report Provides Mixed Picture

- Payrolls climbed 261,000 in October vs Expectations of 205,000 (Beat)

- Unemployment Rate rose to 3.7% vs Expectations of 3.5% (Miss)

Though subtle, the US labour market is starting to show initial signs of fragility. In its latest release, October’s monthly payroll report surprised on the upside through the addition of 261,000 employees. However, this gain in payrolls has been the smallest since the end of 2020. Importantly, while demand seems to be petering off and hiring practices are slowing, Fed officials remain a considerable distance away from attaining success in bringing down inflationary pressures stemming from the labour market.

STOCK MOVEMENT

Stocks making the biggest moves this week:

Uber (UBER) jumped 12% after the company reported stronger-than-expected earnings alongside an upbeat guidance

Abiomed (ABMD) skyrocketed 50% after announcing its agreement to be acquired by Johnson & Johnson for $16.6 billion

Tupperware Brands (TUP) plunged 41% on poor Q3 results due to soft overall sales force activity and poor demand

Etsy (ETSY) soared 14% having beat revenue expectations while issuing an upbeat Q4 guidance

Atlassian(TEAM)cratered 29% as it reported poor earnings that missed expectations alongside an underwhelming outlook

ECONOMIC CALENDAR

1、Economic Events

|

Date |

Events |

Previous |

Forecast |

|

7 Nov |

CN Balance of Trade OCT |

$84.74B |

$91B |

|

9 Nov |

CN Inflation Rate YoY Oct |

2.8% |

2.6% |

|

10 Nov |

US Inflation Rate YoY OCT |

8.2% |

8.1% |

|

US Core Inflation Rate YoY OCT |

6.6% |

6.7% |

|

|

11 Nov |

US Michigan Consumer Sentiment Prel NOV |

59.9 |

59.3 |

2、Earnings Calendar / EPS Forecasts

Disclaimer

This article is intended for general circulation and educational purpose only and does not take into account of the specific investment objectives, financial situation or particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of the investment products mentioned. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product in question is suitable for you.

Past performance figures as well as any projection or forecast used in this article, are not necessarily indicative of future performance of any investment products. Your investment is subject to investment risk, including loss of income and capital invested. The value of the investment products and the income from them may fall or rise. No warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this article. Overseas investments carry additional financial, regulatory and legal risks, you should do the necessary checks and research on the investment beforehand.

The information contained in this article has been obtained from public sources which the uSMART Securities (Singapore) Pte Ltd (“uSMART”) has no reason to believe are unreliable and any research, analysis, forecast, projections, expectations and opinion (collectively “Analysis”) contained in this article are based on such information and are expressions of belief only. uSMART has not verified this information and no representation or warranty, express or implied, is made that such information or Analysis is accurate, complete or verified or should be relied upon as such. Any such information or Analysis contained in this presentation is subject to change, and uSMART, its directors, officers or employees shall not have any responsibility for omission from this article and to maintain the information or Analysis made available or to supply any corrections, updates or releases in connection therewith. uSMART, its directors, officers or employees be liable for any or damages which you may suffer or incur as a result of relying upon anything stated or omitted from this article.

Views, opinions, and/or any strategies described in this article may not be suitable for all investors. Assessments, projections, estimates, opinions, views and strategies are subject to change without notice. This article may contain optimistic statements regarding future events or performance of the market and investment products. You should make your own independent assessment of the relevance, accuracy, and adequacy of the information contained in this article. Any reference to or discussion of investment products in this article is purely for illustrative purposes only, is not intended to constitute legal, tax, or investment advice of any investment products, and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products mentioned. This article does not create any legally binding obligations on uSMART. uSMART, its directors, connected persons, officers or employees may from time to time have an interest in the investment products mentioned in this article.