Global

Global Singapore

Singapore Hongkong

Hongkong Group

GroupUS Macro Strategy Weekly Report – 9 Oct 2023

By James Ooi/ uSMART Market Strategist

Over 13 years of experience in buy-side and sell-side of capital markets

Former Fund Manager of renowned asset management firm

Focus on fundamental analysis and macro-outlook for US & Singapore markets

SGX Academy trainer

This Week’s Market Outlook:

- Last week, SP500 continues its volatile sessions as we saw sp500 dipped to 4229 on Tuesday before closing the week at 4308.

- The significant economic data for this week includes the release of the September Producer Price Index (PPI) and the minutes of the FOMC meeting on Wednesday. Additionally, the September Consumer Price Index (CPI) and Core CPI will be reported on Thursday.

- Monday is Columbus Day, which means banks and the bond market are closed. However, the US stock market remains open, albeit with potentially lower trading volume and increased volatility due to the Israel-Gaza conflict.

- As of the time of writing, both Brent and WTI Crude Oil have surged by 4% following Hamas' unexpected attacks on Israel over the weekend. In a broader sense, it is anticipated that the Israel-Hamas conflict will result in an oil price spike, an uptick in the US dollar index as a safe-haven currency, and an increase in the stock prices of defense (military) and oil-related companies.

- This week's significant earnings announcements feature Pepsi on Tuesday, Delta on Thursday, and Blackrock, JP Morgan, Citi, Wells Fargo, and UnitedHealth on Friday.

- In the past three months, most sectors have experienced corrections, as depicted in Figure 1. Currently, the sectors that have sustained gains of over 10% year-to-date include Consumer Discretionary (+25%), Technology (+36%), and Communications (+40%). While these three sectors do not necessarily need to see further price increases, the remaining eight sectors just need to regain some lost ground to propel the S&P 500 higher in the final quarter.

Figure 1: S&P Sectors Monthly Performance

Source: uSMART, Bloomberg, 6 Oct 2023

The curious case of negative equity risk premium:

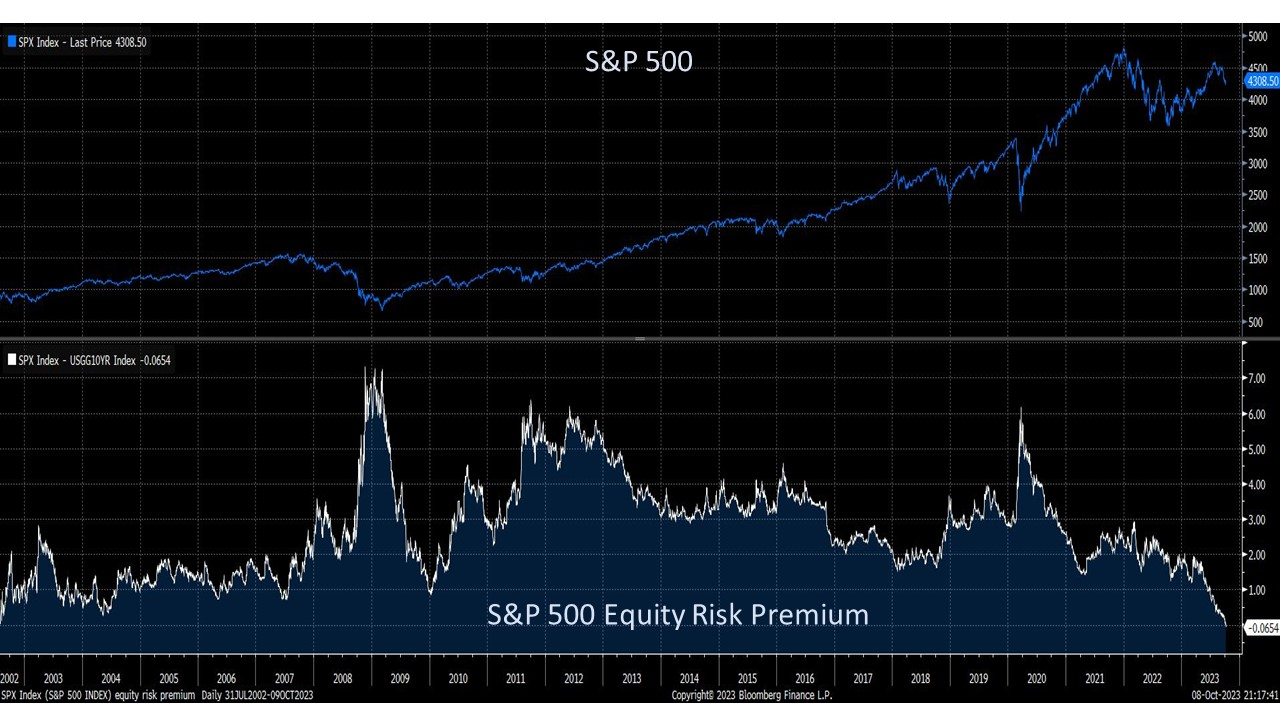

- In theory, stocks are considered riskier assets and are therefore anticipated to offer higher returns than risk-free government bonds, resulting in a higher equity risk premium. Unfortunately, this isn't always the case, as the equity risk premium is currently trading at -0.06%. This means the anticipated return on stocks is lower than that of a risk-free asset. Remarkably, the equity risk premium has not fallen below 0% since July 31, 2002 (Figure 2).

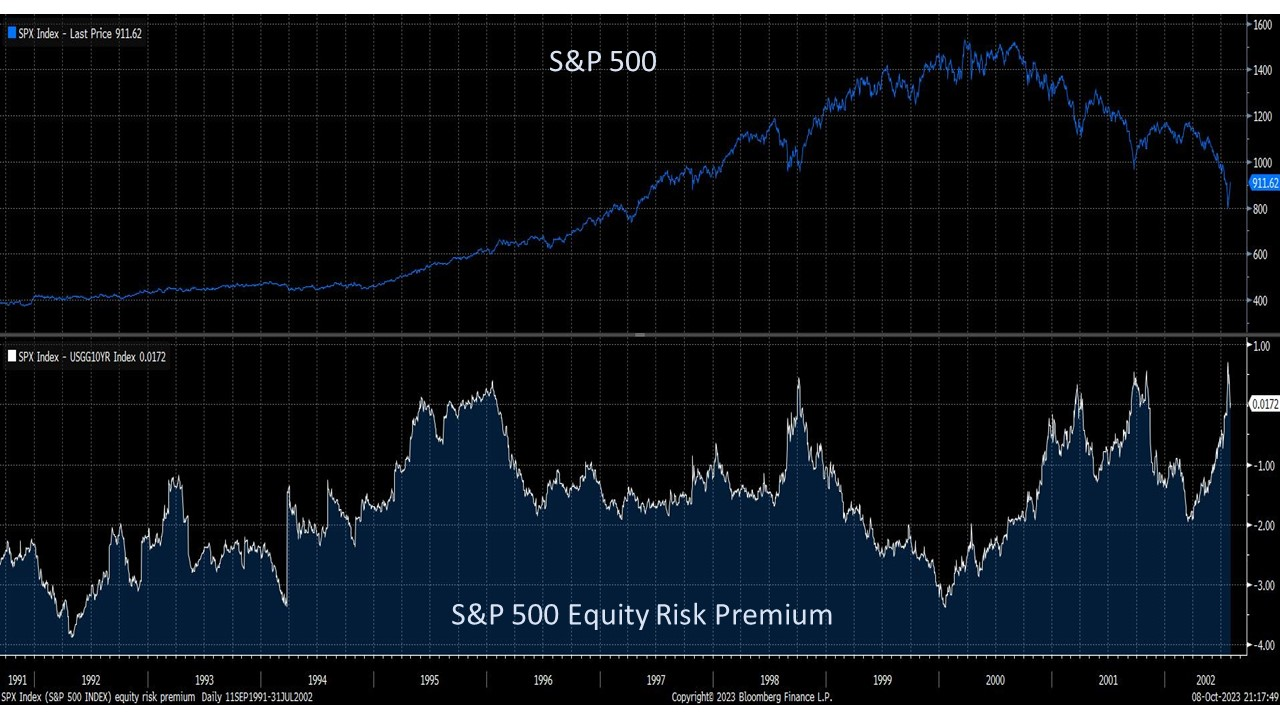

- Modern financial wisdom advises us to favor stocks over bonds only when the equity risk premium is high. Typically, we prefer equities when the equity risk premium exceeds 4%. Thus, the present negative equity risk premium suggests that stocks are unattractive. However, this doesn't imply that US stocks cannot rise further. During the period from September 1991 to July 2002, the equity risk premium stayed below 0%, averaging at -1.64% (Figure 3). Despite this, the S&P 500 experienced significant upside throughout the 1990s, only beginning to correct in 2000.

- We reckon one possible scenario that could lead to a higher equity risk premium is a decrease in bond yields, rather than a decline in stock prices , due to interest rates nearing or already being at terminal levels.

Figure 2: S&P 500 vs Equity Risk Premium (since Aug 2002)

Figure 3: S&P 500 vs Equity Risk Premium (Sept 1991 to Jul 2002)

Source: uSMART, Bloomberg, 6 Oct 2023

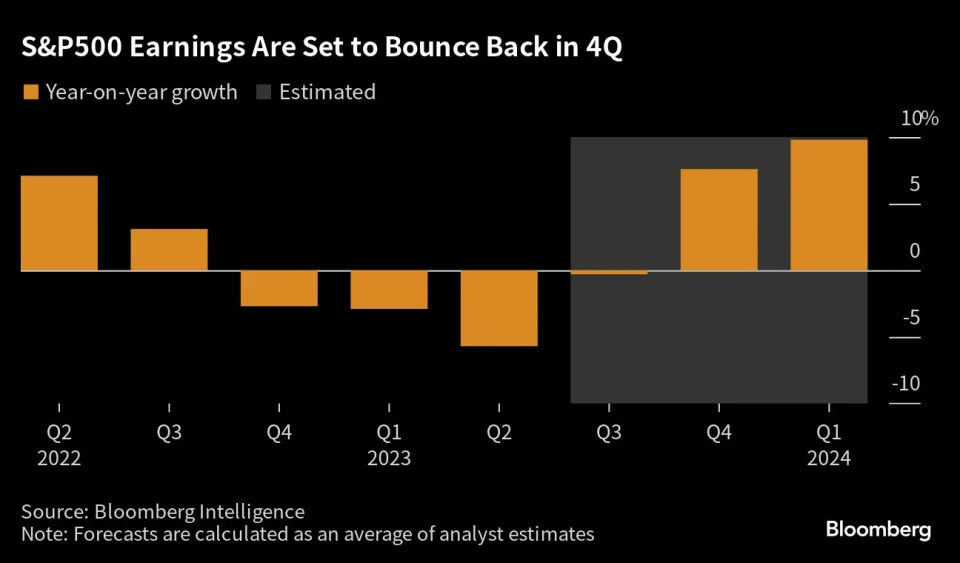

- If earnings year-over-year (YoY) growth is a good indicator of the market bottom, the current consensus earnings YoY expectations suggest that earnings bottomed in Q2 (Figure 4). Hence, stocks could have already reached their bottom.

Figure 4: S&P 500 Earnings growth YoY

Source: Bloomberg, 6 Oct 2023

- In conclusion, our long-term bullish outlook persists.

- Holding a bullish perspective proves challenging given the current elevated levels of interest rates and the US dollar index. Investors could only shift towards optimism confidently when there is a significant decline in both the 10-year bond yield and the US dollar index.

- We may witness higher rates and US dollar index in the near term, but we anticipate that investors could frontload their bullishness into the stock market once they begin to see Q3 earnings surpassing expectations. This expectation stems from the fact that most analysts believe they have already witnessed the worst year-on-year decline in Q2 earnings. Therefore, we believe October could present an opportune entry point for investments. Our preferred investment strategy remains allocating at least 70% of funds into the market to avoid missing out on potential market rebounds.

【Follow us】:

Find us on Twitter, Instagram, YouTube, and TikTok for frequent updates on all things investing.

Have a financial topic you would like to discuss? Head over to the uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimer:

This article is intended for general circulation and educational purpose only and does not take into account of the specific investment objectives, financial situation or particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of the investment products mentioned. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product in question is suitable for you.

Past performance figures as well as any projection or forecast used in this article, are not necessarily indicative of future performance of any investment products. Your investment is subject to investment risk, including loss of income and capital invested. The value of the investment products and the income from them may fall or rise. No warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this article. Overseas investments carry additional financial, regulatory and legal risks, you should do the necessary checks and research on the investment beforehand.

The information contained in this article has been obtained from public sources which the uSMART Securities (Singapore) Pte Ltd (“uSMART”) has no reason to believe are unreliable and any research, analysis, forecast, projections, expectations and opinion (collectively “Analysis”) contained in this article are based on such information and are expressions of belief only. uSMART has not verified this information and no representation or warranty, express or implied, is made that such information or Analysis is accurate, complete or verified or should be relied upon as such. Any such information or Analysis contained in this presentation is subject to change, and uSMART, its directors, officers or employees shall not have any responsibility for omission from this article and to maintain the information or Analysis made available or to supply any corrections, updates or releases in connection therewith. uSMART, its directors, officers or employees be liable for any or damages which you may suffer or incur as a result of relying upon anything stated or omitted from this article.

Views, opinions, and/or any strategies described in this article may not be suitable for all investors. Assessments, projections, estimates, opinions, views and strategies are subject to change without notice. This article may contain optimistic statements regarding future events or performance of the market and investment products. You should make your own independent assessment of the relevance, accuracy, and adequacy of the information contained in this article. Any reference to or discussion of investment products in this article is purely for illustrative purposes only, is not intended to constitute legal, tax, or investment advice of any investment products, and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products mentioned. This article does not create any legally binding obligations on uSMART. uSMART, its directors, connected persons, officers or employees may from time to time have an interest in the investment products mentioned in this article.